계량경제학

11.16 -1

110

2021. 11. 16. 20:33

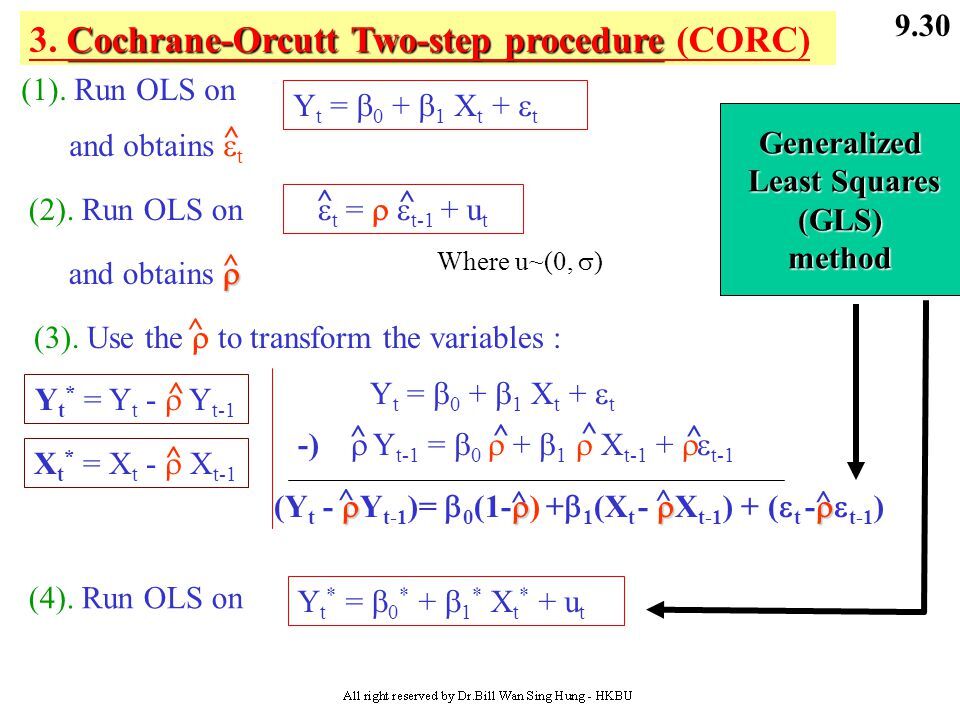

rho가 아니라 rho의 추정량, rho hat이 와야함.

Note

① DW Test is valid only for AR(1).

② DW Test is invalid when a lagged dependent variable is included as a regressor.

③ DW test prone to reject H0.

④ LM: flexible

시계열 데이터의 size를 n대신 T로 표시

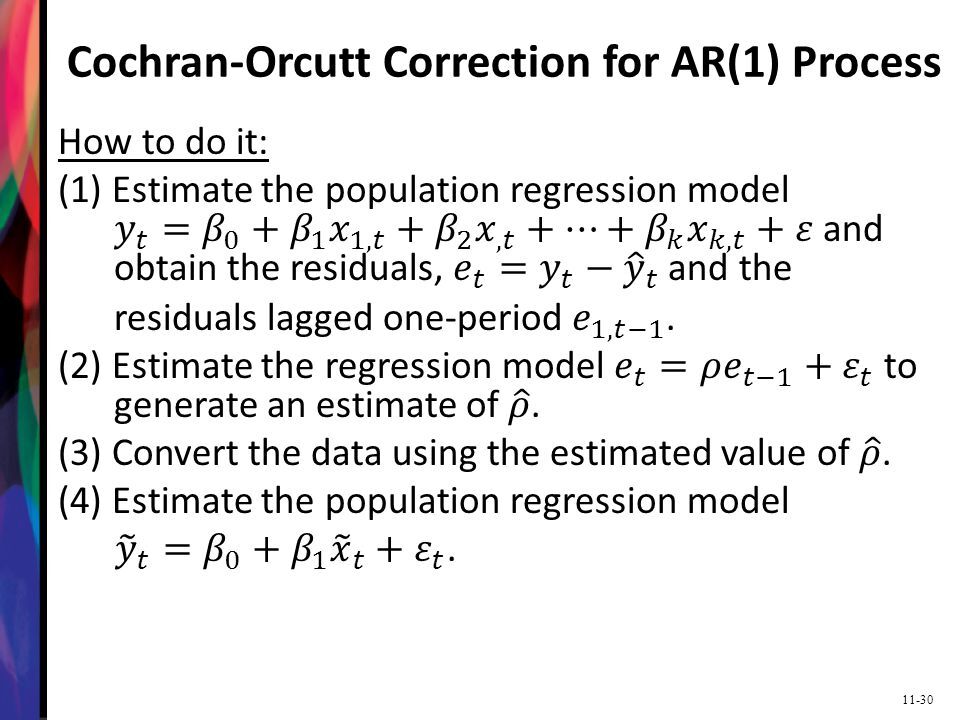

The second step is FGLS based on (20-25)–(20-28). This is the

Prais andWinsten (1954) estimator. The Cochrane and Orcutt (1949) estimator (based

on computational ease) omits the first observation. p.967

AR(1) DISTURBANCE